The gym member needs pyramid: why most fitness operators are leaving revenue on the table

by Natalia Karbasova, Industry Leader, RiminiWellness 2026

Most gyms still sell against two motivations: lose weight and build muscle. Their entire value proposition, pricing, marketing, and programming is built around functional fitness. And for decades, that worked.

But the market is moving. Fast.

"The fitness industry and the longevity industry are merging," says Johannes Kraus, co-founder of YOU(th), a Munich-based digital health startup bringing smartphone-based biomarker screening to gyms and insurers. "I don't see this as two separate industries anymore." The data backs him up: according to a Forbes Health survey, 81% of U.S. adults are willing to invest financially in exchange for a longer, healthier life. Gen Z leads the pack, reporting an average willingness to spend nearly $8,000 per year on their health. And McKinsey's 2025 Future of Wellness report found that Gen Z and millennials already account for 41% of annual U.S. wellness spending despite representing only 36% of the adult population, with nearly 30% saying they prioritize wellness "a lot more" than just a year ago.

The question is no longer whether the fitness industry is changing. It is how to capture the value that sits above the gym floor.

A new framework for gym revenue

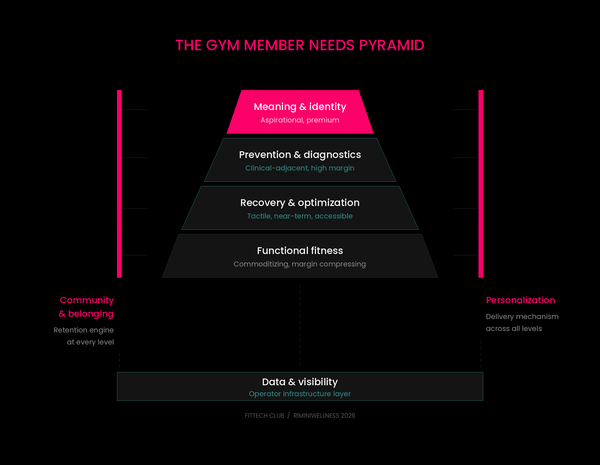

To make sense of this shift, we developed the Gym Member Needs Pyramid, a framework that maps what members actually want from their gym today against the revenue opportunities each level creates.

The model draws on conversations with six international fitness leaders from RSG Group, Trouble Global, Mio Clubs, YOU(th), Garmin Health, and Zing Coach. What emerged is a hierarchy of member needs that goes well beyond physical transformation, and a clear message: the operators who move first will own the next wave of value.

Level 1: Functional fitness - the base is commoditizing

This is still where most members start. Strength training, cardio, flexibility, general health. Every gym in the world serves this level.

The challenge is that technology is compressing the margins at this layer faster than most operators realize. Anton Marchanka, CEO of Zing Coach, has watched this shift from the inside: "The combination of AI and wearables is delivering medical-grade training insights to ordinary gym-goers at a fraction of the cost. What required an entire medical team twenty years ago, we can now deliver with phones and watches at a very low price."

Meanwhile, operators are flying blind. "As a gym operator, you often don't know what's going on," Marchanka observes. "You don't know how people are performing. You don't know if they're progressing. You don't know what their goals are. The only thing you can do is ask them directly or assign a personal trainer." That blind spot is not just an operational gap. It is the reason most gyms cannot serve any level of the pyramid beyond the base.

Level 2: Recovery and optimization - the near-term opportunity

Recovery is the most immediately actionable layer above functional fitness. Sauna, red light therapy, pressotherapy, guided breathwork. Members understand it intuitively. It is tactile, experiential, and increasingly expected.

Jörg Fockenberg, VP of Strategy, Expansion and Franchise at RSG Group, one of Europe's top three fitness operators, is clear about where the opportunity sits: "Recovery entering gyms is the real near-term play. It's more tangible and more immediately actionable than the social wellness trend it is often lumped with."

But he is also clear about what does not work. On the cold plunge trend sweeping social media, Fockenberg is blunt: cold exposure without prior heat is physiologically counterproductive to muscle growth, which is still the primary reason most members join a gym. "I've seen venues do three full sauna-to-cold rounds in one hour. That's borderline bodily harm." His advice to operators: recovery yes, but follow the science, not the hype.

Naomie Martin, co-founder of Mio Clubs in Mallorca, has built her entire model around this layer and beyond. Every member at Mio gets access to private recovery suites, bookable through the app, completely personal. "It's not a shared space. You book it, it's all for you." For operators evaluating where to expand first, recovery is the lowest-barrier entry point into the upper layers of the pyramid.

Level 3: Prevention and diagnostics - clinical-adjacent, higher margin

This is where the fitness industry begins to intersect with healthcare. Biomarker screening, health risk assessments, diagnostic checkups, personalized prevention plans.

Johannes Kraus sees gyms as the natural vehicle: "Gyms have the distribution already to the masses. Right now, longevity is mainly private expensive clinics with fancy products. Gyms are an excellent place to bring longevity to a broader audience." His company, YOU(th), enables exactly this: a two-minute phone-based screening that measures over 50 biomarkers without needles or specialized hardware, creating personalized recommendations that can redirect members to the right service, whether that is a strength session, a doctor visit, or a nutrition plan.

For operators, the positioning challenge is real. As Kraus puts it: "The major barrier is finding the right sweet spot - premium enough to be credible in the longevity space, but not so high-end that the market becomes too small."

The key distinction between this layer and recovery: recovery is something members feel immediately. Diagnostics and prevention are something they understand over time, as year-over-year data reveals patterns, risks, and progress. Both are valuable. They serve different buyer mindsets and price points.

Level 4: Meaning and identity - the top of the pyramid

Some operators are already reaching for this level. Naomie Martin designed Mio Clubs around a philosophy that goes far beyond fitness: "It's your second home, close to your home. A place to train your mental health, your physical health, and your community." Her clubs are deliberately small, 350 square meters maximum, located within 200 to 800 meters of where members live. The programming includes everything from strength training to cortisol reduction sessions, but also a bar designed as a community space. "It's a place to have coffee, to work, to connect with other people, to cry, to smile, or to do nothing."

At Mio, every member co-creates a personalized longevity ritual during a 30-minute onboarding session. "Your longevity is not the same as my longevity," Martin explains. A ritual might include two training sessions, one recovery session with red light therapy, a nutrition protocol, and attending one community event per week, all managed through the app. It is wellness as a lifestyle system, not a gym membership.

This is where premium positioning lives. As functional fitness becomes a commodity, the operators who give members a reason to stay beyond the workout will own the relationship.

The two vertical enablers

The pyramid has four horizontal levels, but it also has two vertical pillars that run through every layer.

The first is community and belonging. Jörn Watzke, Senior Director of Global B2B Sales at Garmin Health, sees community as the deciding factor in whether any fitness product survives: "The app must trigger engagement and create real binding. I must have my community and I must feel personally addressed." Operators, he argues, have a massive built-in advantage. "The customer is already there, already coming in. A standalone app gets installed and deleted quickly. But when it is embedded in the gym experience, the stickiness is dramatically higher."

Emma Barry, founder of Trouble Global and internationally recognized as one of the most influential voices in boutique fitness, sees an even deeper force at work. She points to what she calls an epidemic of loneliness reshaping consumer expectations. People are not just looking for a workout. They are looking for a place to belong. For operators, this is not a soft trend. It is a structural shift in why people choose one gym over another, and more importantly, why they stay. The gyms that build real community into the experience, not as an add-on but as a core part of the product, will have a retention advantage that no amount of equipment or programming can replicate.

Barry also flags a development that is quietly reshaping demand at the base of the pyramid: GLP-1 weight loss drugs are now available in pill form, backed by massive pharma marketing budgets and celebrity endorsements. The direct consequence for fitness operators is that strength training becomes medically essential, because muscle loss is a known side effect of these drugs. "This is going to be shaped by medical systems and who pays for what," Barry observes. For gym owners, it means a new wave of members who are not coming for aesthetics but for medical necessity, and that demands a different conversation, a different onboarding, and a different product.

The second vertical is personalization. Every speaker in every segment, from AI coaching to wearable data to boutique wellness, described the same shift: members expect experiences built for them, not for a demographic group. Whether that personalization comes from algorithms (as Zing Coach delivers through AI-generated training plans adapted to individual wearable data) or from a human onboarding ritual (as Mio does in person) is a design choice. That it needs to exist is not.

The infrastructure underneath

None of this works without data. Most gym operators today have almost zero visibility into what their members actually do, how they progress, what their goals are, and whether they are reaching them.

Jörn Watzke sees a massive wave of technology aiming to close this gap. Garmin Health's ecosystem already connects with several thousand companies building on its platform. But he also sees a shakeout coming: "There is an explosion of coaching apps right now. It has increased five to tenfold. Over 90% will disappear again." The reason is simple: AI has made it trivially easy to build an app that pulls wearable data and returns coaching. But there are not enough customers for all of them.

The operators who invest in their own data infrastructure now, whether by partnering with a platform, adopting a white-label solution, or building in-house, will be the ones who can actually deliver on the promise of every layer above.

As Fockenberg summarizes it: "Nobody knows yet what the studio of the future looks like. But operators should start experimenting with health and technology integrations now, rather than waiting for a clear blueprint."

What this means for operators

The framework is not a prescription. Not every gym needs to offer diagnostics. Not every studio needs a sauna. But every operator should be able to answer one question: which level of the pyramid am I serving today, and where is my next revenue opportunity?

On May 29 at RiminiWellness, we are bringing these six international industry leaders on stage to unpack this framework in practice. The workshop "From Memberships to Meaning" runs from 11:00 to 13:00 on the B2B stage, followed by 30 minutes of direct networking with expert tables where attendees can go deeper with each speaker on the topics that matter most to their business.

Register for your free Rimini here

And sign up to join the workshop

Altre news correlate

30/01/2026

AI nel Fitness: Rivoluzione o Scorciatoia?

06/03/2026

Allenamento isometrico della forza

17/02/2026

Allenarsi senza pavimento pelvico: il limite invisibile dello sport moderno

22/01/2026

Fitness è Scienza, Salute e Prevenzione

03/03/2026

From Wearables to Workflows: How AI and Data Are Redefining the Fitness Studio of Tomorrow

16/02/2026

Il potenziale nascosto nel cassetto

06/02/2026

Lo sport non è bianco o nero: è molto di più

20/01/2026

Longevity is now mainstream, and gyms must choose

05/03/2026

Medical-grade diagnostics are entering the consumer space in Europe

24/02/2026

Nutrizione anti-age

23/02/2026

Schiena e dolore: 5 falsi miti da sfatare

02/02/2026

Scoliosi idiopatica: riconoscerla in tempo cambia tutto

29/01/2026

Strategie nutrizionali per endurance

15/01/2026

Subscription Models, Smart Scheduling & Scalability

09/02/2026

Turismo del benessere: un nuovo modo di vivere l’ospitalità

12/11/2025

Valutare la composizione corporea: from the lab to the field